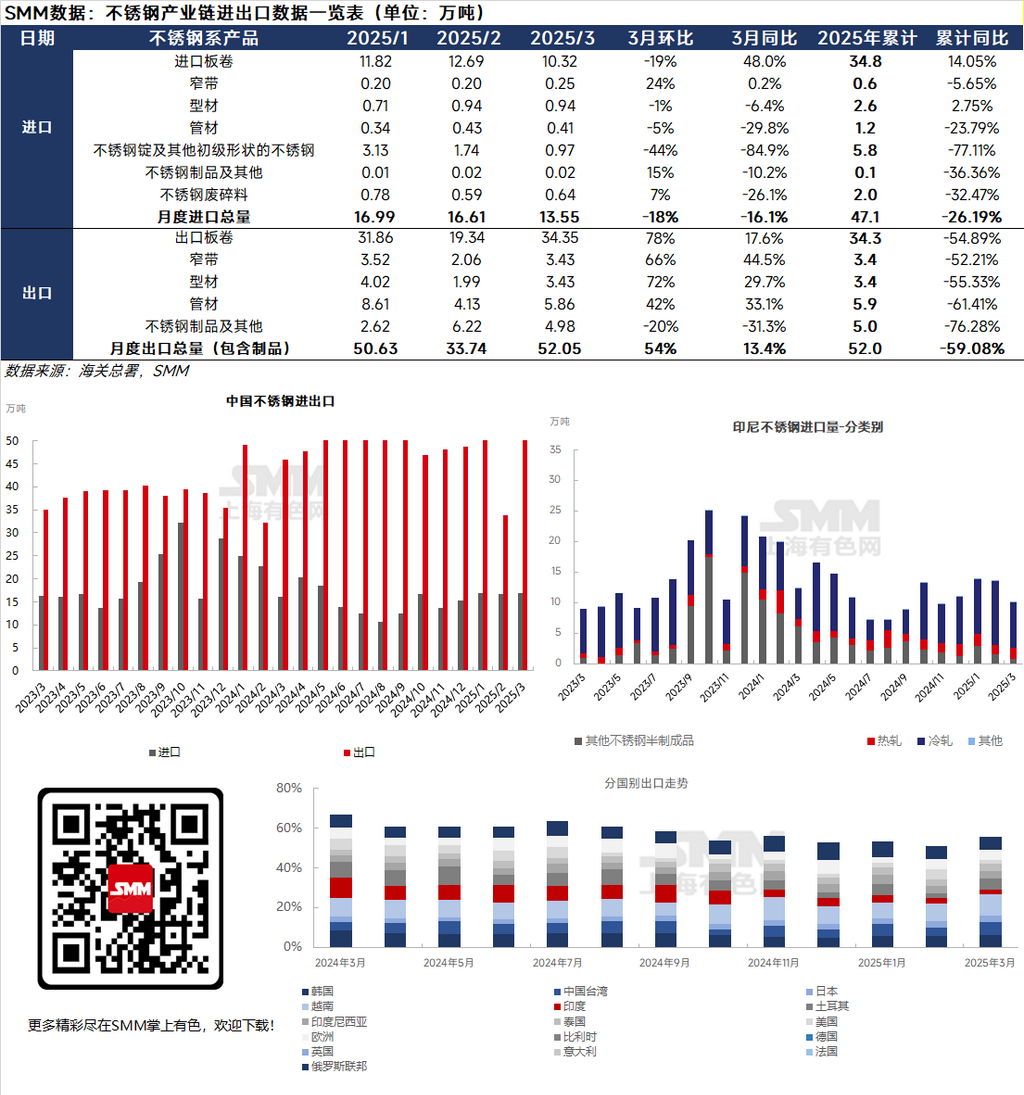

Imports:

SMM statistics showed that China's stainless steel imports in March 2025 stood at 135,500 mt, down 18% MoM and 16.1% YoY. Among them, imports from Indonesia (excluding scrap) totaled 100,700 mt, down 18.05% YoY and 25.82% MoM. By product form, the structure of stainless steel reflow from Indonesia in March showed differentiation: hot-rolled volume increased 14.61% MoM to 17,200 mt, while cold-rolled volume plummeted 28.06% MoM to 74,900 mt, and semi-manufactured products dropped 49.62% MoM to just 8,200 mt. Despite March being the traditional peak consumption season of "Golden March and Silver April," domestic downstream end-use demand did not significantly recover, coupled with a substantial increase in local stainless steel production, leading to a noticeable contraction in imports.

Exports:

Data showed that China's total stainless steel exports in March 2025 surged to 520,500 mt, up 54.24% MoM, returning to a high level above 500,000 mt, and up 13.41% YoY. By product structure, the share of coil exports significantly increased to 65.99%, while the share of products and other categories dropped to 9.58%. All sub-categories achieved substantial growth, with coils, narrow strips, profiles, and pipes up 77.62%, 66.02%, 72.35%, and 41.74% MoM, respectively. By export destination, Taiwan, China, Turkey, and Vietnam became the main contributors to the increase, with exports to Taiwan up 20,400 mt (152.36% MoM), to Vietnam up 28,500 mt (97.42% MoM), and to Turkey up 18,600 mt (225.26% MoM), making the overall export data impressive.

After the Chinese New Year, the peak consumption season of "Golden March and Silver April" began, leading to a concentrated release of pent-up procurement demand. Meanwhile, domestic stainless steel production in March reached 3.4 million mt, with ample supply supporting export growth. Additionally, rising prices of raw materials such as high-grade NPI and high-carbon ferrochrome pushed up stainless steel costs, and the market sentiment of "rush to buy amid continuous price rise and hold back amid price downturn" was strong, further stimulating transactions. However, entering April, US President Trump proposed a significant increase in tariffs on China, posing a major impact on the export-oriented stainless steel industry, spreading market pessimism and causing prices to pull back. Although there are currently re-export trade routes and the actual impact of tariff policies has not fully materialized, the export outlook has been clouded by uncertainty.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)